Does Silver’s Second Act Bring Back Into Play Old Tailings?

Could Tailings Projects Outrun New Mines??

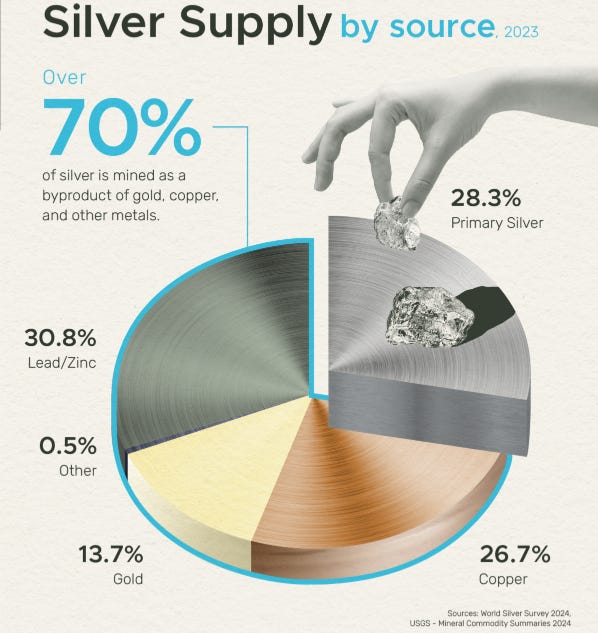

Silver is primarily produced as a by-product of base metal mining operations such as copper, lead, and zinc. Majority of the world’s primary silver mines are concentrated in a handful of countries, particularly in Latin America. Mexico is the most important country in the world for primary silver production. It has been a silver powerhouse since the 1500s and continues to host the largest number of pure silver operations.

Silver: The Unsung Hero of the New Economy - Visual Capitalist

Silver Prices Create a New Narrative for Tailings.

In October 2025, silver broke above the 50 year resistance level of $50 USD which was already touched 2 times throughout that 50 year trend. Silver was at $15 in early 2020 and is now hovering as I write this between $75-$80usd. It made a All Time High of $122usd in early 2026. With many expectations and silver price outlooks of $250+ usd by 2030, silver tailings become lucrative, and a new opportunity never seen for silver mining. This is where the opportunity to turn historic tailings into tomorrow’s silver supply becomes possible and investable. These forgotten silver stockpiles — discarded as tailings decades ago — represent a compelling opportunity today. Throughout most of the last century, silver traded at uneconomical levels: typically below $6/oz before 2000 and often under $4/oz prior to the 1970s. With such depressed prices, miners had little incentive to recover lower-grade silver, leading operations to dispose of tailings piles while leaving behind meaningful quantities of the metal. Today’s prices flip the script.

The Low-Capex Opportunity Hiding in Plain Sight

Silver’s forgotten stockpiles and why tailings matter now represent one of the most pragmatic plays in the critical minerals space. Legacy tailings from Canada’s historic silver-rich districts—such as Cobalt-Gowganda in Ontario—contain millions of ounces left behind by outdated recovery methods. Fast track to production is the name of the game now to take advantage of silver prices. This leads to shorter timelines and why tailings projects could outrun new mines. Conventional greenfield mining projects face a minimum 15 year timeline and hundreds of millions in capital expenditure for exploration, permitting, and build-out. Tailings reprocessing compresses this dramatically. The material is already on surface or near existing infrastructure. Typically these projects are a fraction of new-mine costs—while early cash flow de-risks expansion.

Another key point to this is Ontario’s Recovery of Minerals regime, introduced in July 2025, accelerates execution with an 80-day fast-track permitting pathway tailored for tailings reprocessing and legacy site remediation. Even the policies are developing in support of this thesis for silver tailings.

Why Silver Tailings Offer a Unique Opportunity for Junior Mining Companies

The opportunity we are seeing is unique, seen for the first time in its history for silver. Small junior exploration companies who may also hold a historical project that left tailings are in a very fortunate position to reframe their strategy to creating a producing and profitable mine. The typical route to production for a junior to de-risk as much as possible is traditionally with lots of exploration and years of licenses/permits applications. All this is thrown out the window with a silver tailings opportunity where infrastructure already exists and an employment base already developed around mining exists. Cobalt town is a perfect example. Many of those communities and towns were built around mining, and is easily leverageable by government to boost economic activity. In no other scenario can a mining project be turned around so quickly and cheaply, while providing an economic boost. Something Canada is very much in need of right now. Government therefore has an incentive to leverage this opportunity.

De-Risk Dilution Fears

To further develop the point of providing a unique de-risking opportunity for shareholders, not only can a company begin generating revenues, but dilution is no longer a risk that can be abused to raise money to explore to prove the projects viability. A small mining company can now leverage that cashflow to self fund their growth and development plan such as exploration and mining. As mentioned before, 15-20 years can be the expected timeline before a new discovery is brought to production and 100’s of millions in expenditure before the first dollar in revenue is generated. That money spent is usually in the form of equity raise, which could heavily dilute the investor base and lead to minimal returns as a consequence, if not executed well. This risk can be mitigated instantly with a tailings project to fund that exploration and drilling through real cashflow. At current silver prices of roughly $75usd, a tailings project of 2 million Silver ounces could generate $150 million usd in revenue. If silver touches that $250usd price expectation, that 2 million ounces of silver is now worth $500 million usd.

Securing Silver Supply from Domestic Legacy Assets

Canada’s primary silver output has declined as byproduct production from base-metal mines matures. Reviving domestic tailings output directly addresses supply security for clean-tech supply chains. The socioeconomic impact amplifies the opportunity. Mature mining communities like in Northern Ontario retain skilled labour forces with decades of institutional knowledge in milling, geology, and safety. Projects leverage existing roads, power, and housing rather than building new camps. Direct processing jobs, supply-chain activity, and tax revenues deliver immediate benefits. Remediation improves local environments and community relations, transforming century-old sites into modern economic engines.

Macro tailwinds remain strongly supportive. Silver’s structural deficits and green-energy demand suggest sustained pricing power above historic averages.

China’s Ban on Sulfuric Acid

A potential development out of Beijing over the next few weeks could be the most consequential supply shock nobody in the silver market is talking about yet, which further adds to the silver tailings thesis.

According to industry reports, China could be set to ban exports of sulphuric acid starting next month. On the surface, that sounds like a chemicals story, but it is not; it is a silver story. The connection nobody is making is that sulphuric acid is the lifeblood of copper mining. The heap leach process, dominant across Chile, Morocco, and Indonesia, works by pouring acid over crushed ore to dissolve the copper out. No acid could mean no copper. China supplied 4.6 million tonnes of it in 2025, with 32% going to Chile alone, and now that supply could be gone.

Less copper mined means less silver produced. Approximately 70% of newly mined silver is a byproduct of copper mining. When copper output slows, silver supply slows with it. The silver market was already running a structural deficit, with 2026 marking the sixth consecutive year demand has exceeded newly mined supply. Now add a structural reduction in byproduct silver from acid-starved copper mines. Industrial buyers who cannot substitute away from silver in solar panels and EVs may find themselves competing for whatever physical metal remains.

Another risk factor that adds further validation to the thesis of why silver tailings are a unique opportunity.

Conclusion

In summary, historical silver tailings projects embody a rare alignment of elevated commodity prices, technological readiness, regulatory support, and community capacity. They deliver faster revenue, materially lower capex, secure domestic supply, and positive economic multipliers precisely when countries like Canada and USA seeks critical-minerals autonomy. As silver maintains its elevated range, the macro case for rapid tailings reprocessing has never been stronger.